Garage tax - types

Property owners pay three types of taxes to the budget:

- on property;

- land;

- income

All types of taxes, rates, tax bases and periods are described in the Tax Code.

The tax rate is a certain percentage of the value of the property. The tax base is the cost of the garage or land. Taxes are paid annually.

Property tax

Property (garage) tax is paid by all citizens of the Russian Federation who own garages. And it doesn’t matter whether it’s a permanent structure or a simple “shell”. If there is a certificate of ownership, then there is an obligation to pay tax.

According to Article 402 of the Tax Code, the property tax base is the inventory value of the garage. The cost is calculated by cadastral engineers and indicated in the cadastral passport. If you want to find out the cost of your garage, order an extract from the Unified State Register from Rosreestr.

The garage tax is calculated as follows: the tax rate is multiplied by the inventory value and the deflator coefficient. The rate cannot be higher:

- 0.1% – if the cost of the garage, multiplied by the deflator, is not higher than 300 thousand rubles;

- from 0.1 to 0.3% – if the cost multiplied by the deflator is from 300 to 500 thousand rubles;

- from 0.3 to 2% – if the cost multiplied by the deflator is above 500 thousand rubles.

The tax rate and deflator coefficient are set by municipalities independently; their amounts can be found on the official websites of regional administrations.

The following are exempt from property tax on a garage:

Please note that the benefit is not provided if the garage is used for business purposes, for example, if it is used for production or repairs.

If you belong to one of the above categories, submit an application to the tax office to apply for benefits before November 1. The application is written once (7th part 407 of article 407 of the Tax Code of the Russian Federation).

The tax is calculated by the tax inspector, who will send you a notice and receipt for payment.

Land tax

It is paid by citizens who own the land with the following rights:

- property;

- unlimited (lifetime) use;

- inheritable lifelong ownership.

If the land is transferred for free use or is rented, then no tax is paid.

The tax is calculated from the cadastral price of the plot, which can be found on the Rosreestr website (public cadastral map). The tax is calculated from the moment the land is registered in the cadastral register.

There is also a benefit for land tax - not a complete exemption from payment, but a partial one: 10 thousand rubles are deducted from the tax base (the cost of the plot), and the remaining amount is multiplied by the rate.

The following are entitled to the benefit:

- heroes of the USSR and the Russian Federation (as well as holders of the Order of Glory);

- disabled people of groups 1 and 2 and disabled children;

- veterans and disabled people of the Second World War and combat operations;

- receiving social benefits prescribed due to exposure to radiation in Chernobyl, at the Mayak Production Association, and the Semipalatinsk test site;

- testers of nuclear and thermonuclear weapons at military facilities;

- patients with radiation sickness or disabled people associated with work at nuclear installations, with nuclear weapons or space technology.

Only some organizations will not pay the tax, and among individuals - only those who belong to the indigenous peoples of the North, Siberia and the Far East in relation to fishing and economic areas.

The tax on land under a garage for pensioners is calculated on a general basis.

The tax rate, according to Article 394 of the Tax Code of the Russian Federation, is set by municipalities, but cannot exceed 1.5% of the cadastral value. The tax is also paid according to a receipt from the tax office until October 1.

Income tax

This is a tax that is paid on purchase and sale transactions, gifts and inheritances. The tax base includes both the cost of the garage itself and the land plot.

When selling a garage, the tax is paid by the seller, the tax rate is 13% of the cost. Tax is not paid in the following cases:

- a garage cheaper than 250 thousand rubles;

- the garage has been owned for more than three years (from January 1, 2020, this period will change).

Please note: a member of the GSK is considered to have acquired ownership of the garage from the moment of full payment of the share, and not from the moment of its registration in Rosreestr (Part 4 of Article 218 of the Civil Code)!

Sometimes tax inspectors assure that the three-year period begins to run from the moment the right is registered and on this basis they calculate income tax. If this is your case, take a notice of tax calculation and go to court to complain! In this case, you have 10 days left from the date of receipt of the notification.

If you are not exempt from tax, the next year after selling your garage, before the end of April, go to the tax office, taking the purchase and sale agreement. There, fill out the declaration and receive a receipt.

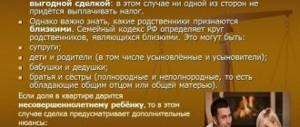

The tax on a gift transaction is paid by the donee. Only close relatives of the donor are not required to pay tax - his better half, children (including adopted children), parents, grandparents, grandchildren, brothers, sisters. All other citizens are required to pay 13% of the cost of the garage to the budget.

When inheriting, the tax will be in the following amount:

- 0.3% of the cost of the garage (but not more than hundreds of thousands of rubles) - for heirs of the first stage;

- 0.6% (but not more than a million) – for the remaining heirs.

Garage tax in shared ownership is paid by co-owners in proportion to their shares.

You have sold a garage that you own. Do I need to pay tax on the income received from the sale of my garage? Are there any benefits for paying taxes? How to declare income from the sale of a garage and how to pay tax? You will find answers to these questions in the article.

Taxes and benefits for garages for pensioners in 2020

If the garage is owned by a community of disabled people, then no tax is paid (disabled people are exempt from land tax). If the plot under the garage is registered as the property of a pensioner, then the Federal Tax Service will annually send him a receipt with the calculated amount.

The procedure for paying land tax will depend on whether the land under the garage is owned by the owner. So, for garages located in a cooperative, the land tax comes to the name of the cooperative. His accountants will then divide the costs between the owners.

When can you avoid paying tax when selling a garage?

In some cases, income from the sale of a garage is not subject to personal income tax (NDFL). This means that after selling it, you may not pay tax at all. Let's consider these cases in more detail.

There are two periods of ownership of a garage, beyond which you may not pay personal income tax on the income received from its sale. These terms are three years and five years.

We immediately draw your attention to the fact that the period of ownership of a garage is determined from the date of state registration of ownership of it. This date is indicated in the certificate of state registration of ownership of the garage (such certificates were issued until July 15, 2020, after which they were cancelled) or in an extract from the Unified State Register of Real Estate.

The minimum period of ownership of a garage is 3 years.

You can take advantage of tax relief on a sold garage (not pay tax at all) after three years of owning it only in cases where:

- you received the garage as a property by inheritance or gift agreement from a family member or close relative;

- or purchased it before January 1, 2020.

The minimum period of ownership of a garage is 5 years.

This tenure period applies to all citizens who own garages, except for those who are subject to the three-year rule (see the previous paragraph). After the specified period (five years), after selling the garage, you can not pay tax on the income received if you purchased the garage after January 1, 2020. It turns out that you can sell a garage without paying tax only after January 1, 2021.

In all other cases of selling a garage, you will not be completely exempt from paying taxes, but you will be able to receive a benefit such as a property deduction. Read more about this in the section below.

Features of income tax

Such a fee is paid if a certain profit is received from the garage. It can be obtained through sale or rental. In this case, it does not matter by what method the object was registered as property.

The size of such a fee is standard and equal to 13% of the profit received for residents, but for non-residents an increased rate of 30% is used.

The funds are paid even if a deed of gift is issued to a non-relative, so the recipient still has a certain income from which a fee is paid, but the seller in such a situation does not pay the funds.

The percentage is set only by the federal government, so local governments cannot lower the rate.

Should pensioners pay garage tax?

If the garage is inherited, then payments are calculated individually, since the price of the object is taken into account:

- if the heirs of the first stage receive the object, then they pay 0.3% of the cost of the structure;

- for other heirs the rate increases to 0.6%, but up to 1 million rubles.

If an object is given to family members, they are exempt from paying this fee.

Such citizens include parents, children or official spouses, as well as brothers or sisters, but they must have common parents with the donor.

How to register a garage as your property? What documents are needed? Detailed instructions here.

Rules for calculating income tax

Income tax is calculated by employees of the Federal Tax Service, and the process is considered to be quite prompt and simple. Payment of the fee must be realized by all citizens, therefore their citizenship and place of residence are not taken into account.

If the property is sold, the seller, represented by the former owner, must pay tax on the income received. However, there are certain situations in which you can obtain an exemption from transferring these funds.

These include:

- the cost of the garage does not exceed 250 thousand rubles;

- its area is less than 50 square meters. m.;

- the garage has been owned by the owner for more than five years, if it was previously purchased, and if it was received as a gift or by inheritance, then more than three years must pass.

People who are beneficiaries are exempt from the fee.

Calculation example

For example, the owner of a garage decides to sell this object, which was purchased 2 years ago for 340 thousand rubles. The size of the structure exceeds 50 square meters. m.

Property for sale for 420 thousand rubles. to strangers. In this case, the amount of the fee will be equal to: (420-340)*13%=10,400 rubles.

Important! If after the sale of an object you still receive notifications from the Federal Tax Service about the need to pay various fees for it, then you need to come to the branch of this institution with an agreement on the basis of which the right to the garage was transferred to another person

Who are the beneficiaries?

When calculating property taxes, the ability of many citizens to benefit from certain benefits provided by benefits is taken into account. They may completely waive payments or provide various discounts.

Changes are regularly made to legislation, on the basis of which more and more people can be considered beneficiaries.

Rules for calculating property taxes, see this video:

These include:

- heroes of the Russian Federation and the USSR;

- disabled people of the first two groups;

- disabled since childhood;

- veterans and participants of the Second World War;

- combat veterans;

- pensioners;

- people involved in eliminating the consequences of the Chernobyl accident;

- military families who have lost their breadwinners;

- military personnel whose service life exceeds 20 years;

- people who have become disabled as a result of the use or creation of military or space technology.

Preferential categories are exempt from paying garage tax.

How to get a tax benefit

If you sold a garage that was in your ownership for less than one of the minimum tenure periods specified in the previous section (the period that suits you), then you will not be completely exempt from paying personal income tax. But on the other hand, when selling a garage, you can reduce the income received by choosing one of two options for reducing income.

You can:

- or reduce income by an amount equal to the cost of the garage, but not more than 250,000 rubles;

- or reduce income by the amount of actual expenses when purchasing this garage, but provided that the expenses are documented.

The key quantity is the income received from the sale. The tax is tied to income. When selling real estate, in particular a garage, there are features related to determining the amount of income. Let's look at the rules for determining income.

Income from the sale of a garage is determined in accordance with the purchase and sale agreement if:

- the garage was purchased by you before January 1, 2020;

- The cadastral value of the garage has not been determined as of January 1 of the year in which state registration of the transfer of ownership of the garage from you to the new owner was carried out.

If you purchased the garage after January 1, 2020, then the income from its sale is determined as follows. The cadastral value of the garage as of January 1 of the year in which the transfer of ownership of it from you to the buyer was registered is multiplied by a reduction factor of 0.7. The resulting value, if it is greater than the amount of income from the sale of the garage under the contract, is taken into account when calculating personal income tax. If the amount received is less than the income under the agreement, then the agreed amount of income is used to calculate personal income tax.

The Tax Code of the Russian Federation allows constituent entities of the Russian Federation to reduce down to zero:

- the minimum maximum period for owning a garage (which, according to the Tax Code, is 5 years);

- the size of the reduction factor by which the cadastral value of the garage is multiplied (the size of the reduction factor established by the Tax Code of the Russian Federation is 0.7).

What does the tax rate depend on when calculating property tax?

A peculiarity of the housing tax compared to other fiscal payments is that the program for transferring it to a unified taxation base according to the Unified State Register has not yet been completed. Land tax has already passed this stage and is calculated according to a uniform methodology throughout the country. And the housing tax will be in a transitional state for another 2 years, divided into 2 calculation methods:

- according to the established BTI (so-called inventory value);

- according to that established by technicians from the SRO (the so-called cadastral value).

The first method is used by the few remaining regions that have not yet had time to massively revaluate property in their territories.

For this reason, the Tax Code of Russia takes into account the calculation method when using cadastral valuation and the calculation method using BTI, preferences for one cost and preferences for the second. Also, the tax rate for property tax for individuals is determined depending on the method of calculation.

But in addition to differences in the method of calculating the tax base, tax rates on real estate for individuals are related to the level of legislation. After all, this tax is local, which means it is established by the local laws of each municipality.

An example of calculating tax with a property deduction for a garage

Let's look at two examples of calculating personal income tax after selling a garage.

Example 1.

The citizen received a garage as a gift from his father in 2020. Subsequently, in 2020, he sold the garage under a purchase and sale agreement for RUB 900,000. In this case, a citizen can apply a property deduction when calculating the personal income tax that he must pay. Please note that after selling a garage, a citizen cannot be completely exempt from paying taxes, since three years have not passed since the garage was donated to him.

The cadastral value of the garage as of January 1, 2020 is 1,100,000 rubles.

If you follow the rules for calculating the property deduction, then the cadastral value of the garage must be multiplied by a reduction factor of 0.7, and then compare the resulting value with the value of the garage under the contract. After this comparison, you need to choose the amount that turns out to be larger. It will be the income from the sale and will be used to calculate personal income tax.

In our case, the value obtained by multiplying the cadastral value by a coefficient of 0.7 (estimated income) is 770,000 rubles. And this value is less than the contract price of the garage, which is 900,000 rubles. Therefore, when calculating personal income tax, you must use the income from the sale specified in the contract, that is, 900,000 rubles.

A citizen can apply a property deduction in the amount of 250,000 rubles to the amount of income under the contract, that is, he can reduce the income under the contract by the specified amount. In this case, the taxable amount of income from the sale of the garage will be 900,000 – 250,000 = 650,000 rubles.

On this amount, the citizen will have to pay personal income tax (13 percent), the amount of which will be 650,000 x 0.13 = 84,500 rubles.

Example 2.

If the citizen from example 1 sold his garage not for 900,000 rubles, but for 500,000 rubles, then with the same cadastral value, the estimated income (770,000 rubles) would exceed the income under the contract. Therefore, when calculating personal income tax, it would not be the income under the contract that would be used, but the estimated income of 770,000 rubles.

After applying the property deduction (250,000 rubles), the amount of taxable income would be 770,000 – 250,000 = 520,000 rubles.

Then the personal income tax would be 520,000 x 0.13 = 67,600 rubles.

How to submit a declaration

If the income you receive from selling your garage is not completely tax-exempt, then after selling your garage and receiving the proceeds from its sale, you must do two things.

First.

You must submit a 3-NDFL tax return to the tax authority. But if the sold garage was purchased by you after January 1, 2016, then you must submit along with the declaration.

You must submit the declaration no later than April 30 of the year following the year in which you received income from the sale of the garage.

You can use any of the following methods for submitting your declaration:

- filing with the tax authority in person or through your representative;

- sending by mail by valuable or registered letter with a list of the contents;

- transmission in electronic form through the Unified Government Services Portal or the taxpayer’s personal account.

Second.

You must remit the tax. You must transfer the calculated personal income tax (NDFL) for the sold garage to the budget no later than July 15 of the year following the year in which you received income from the sale of the garage.

Property tax must be paid by all persons who own real estate. The Federal Tax Service periodically sends notifications or transmits them to the local administration. Failure to receive a letter from the tax service does not relieve the garage owner from the obligation to make payments on time.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how to solve your specific problem

— contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week

.

It's fast and FREE

!

If this is not done, then tax liability in the form of payment of penalties for each day of delay and a large fine is possible. There is an annual tax that is paid for the fact that the garage is simply owned by an individual or company. It is also necessary to make tax payments if the owner of the garage decides to sell it and.

The transaction tax takes into account the status of the payer, the period of ownership of the property, and the possibility of obtaining a property deduction.

What land tax benefits are available to labor veterans?

- The inspectorate will tell the labor veteran who applies whether he is a beneficiary on this basis or not. Of course, for this you will need to present one of the documents confirming this status. In the event that the applying citizen can still claim a benefit, he must write an application for its provision and submit it to the tax office.

- In addition, every year all tax payers receive notifications from the inspectorate with the amount of tax due.

- If for some reason the beneficiary missed the deadline for assigning a benefit in the form of a reduction in the tax base, he can apply to the Federal Tax Service with an application to recalculate the tax amount, but only for the last 3 years. The recalculated part of the amount from it will be in the personal account of the taxpayer, and payments will be made from it towards other taxes.

We recommend reading: Latest news about the liquidators of the nuclear power plant in Sevastopol for 2020

What do you need to know?

If the payer receives a notification, then the amount of tax, as well as benefits, is calculated by a specialist. The inventory value of the garage is taken into account.

If the property value is at least 300 thousand rubles, you need to pay 0.1% property tax. If the cost of a garage is 300-500 thousand rubles, then the rate varies in the amount of 0.1-0.5%.

When the property price is over 500 thousand rubles, the cost of non-residential premises is 0.5-2%. When selling a garage or donating it, you must pay income tax, which is 13% of the amount received as a result of the alienation of the property.

Garage tax must be paid. Payments are transferred to the municipal budget. The amount is calculated individually, depending on the value of the property.

The amount is paid by the property owner himself, i.e. There are no intermediary tax agents when making payments.

Garage tax as a payment for property must be distinguished from income tax, which is paid after a real estate transaction. In the first case, it is calculated depending on the value of the property, in the second - on the amount of funds received after the transaction.

general information

If real estate belongs to several citizens who are related to each other, then each owner is obliged to pay his part of the tax.

A notice for payment of tax, which specifies the procedures and deadlines for payment, is issued to the owner of the garage by the relevant tax authority operating at the location of the property.

Real estate tax is a local contribution, which is credited to the budget at the location of the payer’s structure.

In this case, the payer is considered to be the owner , who can be either a citizen of our state or a foreigner.

garage tax rate The inventory value of real estate is considered to be its cost, taking into account the wear and tear of building materials and the costs of their acquisition, which were used in the construction of the garage.

The tax rates in question depend on the established inventory value. If the total inventory value of the garage is less than 300 thousand rubles , then the garage tax rate will not exceed 0.1%, from 300 to 500 thousand rubles - the real estate tax rate will be in the range from 0.1 to 0.5 percent. If the total cost of inventory is above 500 thousand rubles , then the garage tax rate will vary from 0.5 to two percent.

Garage tax

It is calculated for each period and is due later than mid-November. If this is not done, the tax service reserves the right to charge penalties and bring the offender to other types of liability.

Separate building

The tax is levied only on garages that are registered with Rosreestr. This can be a permanent building or a garage, which is located in the household and is considered a separate piece of real estate.

Payments for an individual building are calculated in accordance with the general procedure. The main condition is that title deeds be issued for the garage.

In a garage cooperative

In 2020, the tax on real estate in a garage cooperative is paid in accordance with the general procedure. The inventory value of the property is determined, and the tax amount is calculated based on its indicator.

It is paid by each member of the cooperative separately, within the time limits established by the Federal Tax Service.

To the ground

It is also transferred to the local budget. It is paid simultaneously with the tax payment for the garage.

The cost of the tax is calculated based on, and amounts to several hundred rubles per year - for a standard plot of 3-4 acres.

When selling

When selling a garage, you need to pay personal income tax if the building has been owned for less than three or 5 years.

You can avoid paying tax when selling a property if the garage has been owned for less than three years and has previously passed to the owner:

- in order ;

- by inheritance;

- as a gift (from a close relative);

- as an object of rent.

If the garage was previously acquired through compensated transactions, then for legal non-payment of tax, it must be owned for at least five years.

To receive a property deduction, the cost of the garage must be at least 250 thousand rubles.

Donation

The recipient of a gift in the form of a garage must pay NFDL in the amount of 13% of the value of the real estate.

The exception is when the garage is donated by a close relative - parents, children, grandparents, brothers and sisters. Then payment of tax will not be required.

Garage

A garage, according to the law, is defined as a non-residential real estate structure. It doesn’t matter what kind of garage a person owns - a permanent one or a shell one, if the owner has a certificate of state registration of property in his hands, he will have to pay property tax.

The garage real estate tax begins to accrue from the moment the property is registered in Rosreestr and amounts to:

- up to 300 thousand rubles (inclusive) - up to 0.1% (inclusive);

- from 300 thousand rubles to 500 thousand rubles (inclusive) – from 0.1 to 0.3% (inclusive);

- more than 500 thousand rubles - from 0.3 to 2.0% (inclusive).

The calculations are based on the inventory value of the property.

Inventory value is the cost of restoring a property, taking into account its wear and tear and rising prices for construction work and products, multiplied by the tax rate (each region has its own). The inventory value of the object is recorded in the technical passport of the garage and is not the cadastral value of the object (the latter is on average 20 times greater than the inventory value).

If the garage was officially rented out, the owner will have to pay two taxes for the garage:

- for the property of individuals;

- income tax (13%).

It will not be possible to shift the property tax onto the tenant's shoulders, because... he is not the owner of the garage.

Filing a declaration

The declaration must be submitted when paying NFDL. The applicant can calculate the tax amount independently. He has the right to take the amount of income received or take into account the cadastral value of the property, taking into account a reduction factor of 0.7% of its value.

You can also take into account the difference between the income received and the cost of the transaction and, taking into account the resulting difference, calculate personal income tax.

The declaration should be submitted directly at the Federal Tax Service office or through the department’s website, having previously downloaded documents in XML format. The document can be submitted in paper form or typewritten.

Possible difficulties

Neglecting to pay taxes can result in penalties of several thousand rubles. If information about the garage was not transferred to the Federal Tax Service Rosreestr, then the tax notification may not arrive at all. Then everything depends on the behavior of the specialists “on the ground”. In this case, non-payment of tax may not occur for years, which does not formally relieve the payer of responsibility.

The Tax Code of Russia stipulates that owners of any type of property are required to pay an annual fee to the state budget. The main objects of taxation are houses, apartments or rooms in communal apartments.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how to solve your specific problem

— contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week

.

It's fast and FREE

!

Russian legislation obliges owners of non-residential real estate for various purposes to make payments. A list of taxes that are payable by owners of garage buildings has also been established.

General information

Taxation is a very labor-intensive process that affects all areas of citizens’ lives without exception, including the use of real estate.

The main objects of taxation are:

- residential real estate;

- technical buildings and so on.

Income tax on a garage building is payable if:

- committing ;

- at ;

- when trying to inherit.

During the sale of a garage building, the seller is required to pay a tax in the amount of 13% (for non-residents of the country - 30%) of the cost, which was specified in the agreement.

The only exceptions are situations in which:

- the cost of the building is less than 250 thousand rubles;

- The seller has owned the garage for more than 3 years.

Important: if the ownership period is calculated in relation to the building located in the GSK, then it should be counted from the period of full payment of the share.

Tax on land under garage

The land tax for a garage building has some nuances. Their knowledge can exclude the possibility of bringing to administrative liability due to non-payment of established tax fees.

Do I need to pay?

Recently, amendments were made to the Tax Code of the Russian Federation in relation to real estate. After calculating the cadastral cost, it is necessary to calculate tax fees. Title: “Tax on real estate of individuals.”

In practice, this type of tax was introduced for capital property in Russia, which determined the cadastral valuation of construction projects.

– state calculation of the market cost of constructed objects.

Property tax, including garage buildings, is used to pay all citizens who own buildings, regardless of whether they are monumental or temporary.

It is important to remember: the property tax base is the inventory cost of the property, which is determined by specialists of the cadastral authority.

Bid

In 2020, there are several options for paying taxes:

- if the garage building is located in the GSK and is registered as the property, but the allotment is not, then the tax must be paid by the cooperative;

- in case of receiving land ownership, a receipt for payment will be received annually (once a year);

- in the case of the construction of a garage building in the GSK, which for some reason is not subject to taxation, then the owners of the garages do not automatically pay the tax.

The size of the tax base directly depends on some important nuances, namely:

- the rate varies by region - the average is 1.5%;

- from the cost of the plot according to the cadastre.

The tax is payable from the period when the land plot begins to be used, and regardless of whether there is already a garage on it or only repair work is being carried out on its construction - you need to pay.

It is necessary to pay attention to the fact that according to Russian legislation, the maximum tax rate on land under a garage is 1.5%.

How to calculate?

Calculating the tax on land under a garage is quite simple. It will be enough to multiply the tax base by the tax rate.

The tax base refers to the cadastral cost of the plot, which is displayed in the cadastral passport.

In order to make a reliable calculation, you can use the built-in online calculator on the official portal of the tax authority. With its help, you can make all the necessary calculations within a few minutes and eliminate the possibility of errors.

The tax on the land under the garage must be paid no more than once a year.

Tax structure and amount

From the point of view of the official classification, the garage tax does not exist as such - it belongs to the category of “property tax for individuals” (apartments, houses, outbuildings, dachas, but not land plots). Therefore, from the point of view of legislation, this payment is divided into 2

- Actually the tax for owning a garage.

- The tax for the ownership (or use) of the land plot located under it is already a land tax.

In some cases, personal income tax will also be added to these payments - for example, the owner decided to rent out his garage for a certain monthly fee. Therefore, in general, the structure of this contribution will look like this.

To the garage

Until recently, the amount of payment was determined based on the inventory value of the building. This value can be found in the technical passport, and if it is missing, you must order an assessment procedure at the local BTI office. The amount is determined by state appraisers, so in most cases the price turns out to be significantly lower than the market price.

However, at the moment, property is valued at the cadastral price, which is as close as possible to the real (market) price. Despite the fact that in some regions they still use inventory value, from 2020 there will be a final transition to cadastral value throughout Russia. Garage tax is paid annually and is determined as a percentage of the amount (see table).

| cost of garage, in rubles | tax amount, % |

| up to 300,000 | up to 0.1 |

| 300 001-500 000 | 0,1-0,3 |

| 500,001 or more | 0,3-2,0 |

To the ground

The size of this contribution depends on several factors:

- If the land is owned, then the owner pays the tax on it. The amount of tax is determined by the cadastral value of the land plot, as well as the tax rate, which is set individually for each region (on average about 1.5%).

- If the site is owned by a garage cooperative (or rented by this organization), then the payment is distributed in equal shares among all members. Relevant documents (receipts) can be obtained from your local accounting office.

Sometimes there are cases that a cooperative is an organization that has the right to significant benefits in paying taxes on garages and land - for example, this is a partnership for the disabled. Then all members of the cooperative have the right to receive such benefits (including those who are not disabled).

For income

This tax is paid only if the owner has rented out the garage or uses it for a commercial purpose (service station, warehouse, etc.). Receipts are also sent by the local branch of the Federal Tax Service, and they are paid separately from other types of garage taxes (property and land).

If the owner is a pensioner

Since the tax amendments entered into legal force, some aspects have been adjusted for citizens of retirement age.

As with other preferential categories, pensioners are exempt from paying taxes exclusively on one category of property.

If the benefit was issued for a dacha, house or apartment - garage building, it is confirmed for taxation according to generally accepted rules.

It is important to remember: if a garage building is exempt from taxation, but is in common shared ownership with citizens who are not of retirement age, then only part of the benefit recipient is exempt from tax.

An additional feature is the cancellation of exemption from taxation of land plots that were allocated for any type of property for the use of pensioners.

At the same time, there is a loophole - the right to provide benefits remains with local governments. In other words, they can legitimize this fact at the regional level.

The mechanism for receiving benefits in 2020 remained unchanged and is as follows:

- You must contact the territorial tax authority at your place of residence.

- You must have all the necessary documentation with you, including your pension certificate.

Important: a copy of the pension certificate must be attached to the completed application.

Garage tax rate in 2020 for individuals

A garage is a full-fledged property - non-residential real estate. The garage tax rate in 2020 is, as before, determined by the municipality. The tax begins to be calculated from the moment the property is registered in the Register and directly depends on the cost of the garage. The cadastral value is taken into account.

As representatives of the Federal Tax Service of Russia explained on their official website, from January 1, 2020, in Moscow, property tax for individuals is calculated based on the cadastral value of real estate.

However, when choosing a garage as an object of preferential taxation, if it is divided into shares and the co-owner is not a pensioner, then you can avoid paying tax only for the part owned by the pensioner. If there is still an opportunity to reduce the cost, you need to fill out an application and contact the tax office with a copy of your pension certificate and passport.

The objects of taxation are immovable things - those that are inextricably linked with the land cannot be moved without causing significant damage. Movable things are not subject to this tax, but can be subject to taxation for other reasons (for example, the owner is required to pay transport tax on a car).