The presence of country property, especially if this property is a cozy cottage with adjacent land, is not only an excellent investment, but also a place for a good, complete rest for a modern resident of a metropolis. In this regard, the high demand for such property in the vast domestic real estate market is quite justified. This trend has not gone unnoticed by the state, and already in 2020, the owners of the above-mentioned property are becoming familiar with a new item of family budget expenditure - the cottage tax. Read more about this in the article.

Features of the new taxation

If before 2020, annual deductions from real estate in favor of the state were calculated based on its inventory value, then with the onset of 2020 the situation has changed. So, today the market value of real estate, or cadastral value, is taken into account when calculating. Such an innovation did not please the owners at all, but, on the contrary, promises some of them to “tighten their belts.”

This is due to the fact that the market value of the property is several times higher than the inventory value, which means the tax amount will be increased.

Another surprise is the tax on cottages and other country property with adjacent land. If, when calculating tax on an apartment, one annual payment is formed, then, in the case of country real estate, the situation is slightly different. According to the law, owners will now be required to pay separately two types of taxes: land and property.

In a year, the tax on houses and dachas could increase 125 times

“It is for this reason that our company was chosen to carry out the assessment work. The BTI archive stores information about about 10 million capital construction projects in the Moscow region. The technical passport, which is in the BTI archives, contains much more information than the State Property Committee. With the help of archives, we supplement the information of the State Property Committee, determine the percentage of wear in order to make the most transparent and honest assessment.

— But in order to use the services of the MFC, you must first register your property, put it on the cadastre, clarify the boundaries of the site, register the house, and “link” it to the site. A lot of fuss. Probably half of the property owners in the Moscow region have not done any of this. And for some - the whole thing.

22 Jul 2020 glavurist 4747

Share this post

- Related Posts

- Transport tax for pensioners in 2020 in the Samara region

- What to do if the documents for the car are lost

- Work under a contract without a work book in Moscow

- Calculation of unemployment benefits in Ukraine in 2020 calculator

Land tax

Persons who are obliged to pay land tax include citizens who own real estate not just on the basis of ownership, but also on the right of perpetual (permanent) use or lifelong inheritable ownership.

Land tax refers directly to such a type as local tax. This means that its payment is made by a private individual in favor of the municipal budget, and the tax has the right to “exist” based on the decision of local authorities. Also, land tax is regulated by the Tax Code of the Russian Federation and local government laws.

As with property taxes, land taxes are calculated based on market value. The tax rate is set by local governments, but there are still limits set by the state, above which the land tax cannot be higher.

According to the law, tax rates cannot be higher than:

- 0.3% of the tax base (agricultural lands, settlement lands used for agriculture, areas of housing stock and engineering infrastructure, areas of personal subsidiary plots and dacha farms, etc.).

- 1.5% in relation to other land plots.

Taxes on residential buildings, dachas, apartments, garages and other buildings

- for an apartment - 20 m2 of the total area of the apartment;

- for a room - 10 m2 of the total area of the room;

- for a residential building - 50 m2 of the total area of the house;

- for a single real estate complex, if it includes at least one residential building or one residential premises - by 1 million rubles.

- Heroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of three degrees;

- disabled people of disability groups I and II;

- disabled since childhood;

- participants in the Civil War and the Great Patriotic War, other military operations to defend the USSR from among military personnel who served in military units, headquarters and institutions that were part of the active army, and former partisans, as well as combat veterans;

- civilian personnel of the Soviet Army, Navy, internal affairs and state security bodies who held regular positions in military units, headquarters and institutions that were part of the active army during the Great Patriotic War, or persons who were in cities during this period, participation in the defense of which these persons are counted towards their length of service for the purpose of granting a pension on preferential terms established for military personnel of active army units;

- persons entitled to receive social support in accordance with the Law of the Russian Federation No. 1244-I of May 15, 1991 “On the social protection of citizens exposed to radiation as a result of the Chernobyl nuclear power plant disaster”, in accordance with Federal Law No. 175-FZ of November 26, 1998 of the year “On the social protection of citizens of the Russian Federation exposed to radiation as a result of the accident in 1957 at the Mayak production association and the discharge of radioactive waste into the Techa River” and Federal Law No. 2-FZ of January 10, 2002 “On social guarantees to citizens exposed to radiation exposure due to nuclear tests at the Semipalatinsk test site";

- military personnel, as well as citizens discharged from military service upon reaching the age limit for military service, health conditions or in connection with organizational and staffing events, having a total duration of military service of 20 years or more;

- persons who were directly involved as part of special risk units in testing nuclear and thermonuclear weapons, eliminating accidents of nuclear installations at weapons and military facilities;

- family members of military personnel who have lost their breadwinner;

- pensioners receiving pensions assigned in the manner established by pension legislation, as well as persons who have reached the ages of 60 and 55 years (men and women, respectively), who, in accordance with the legislation of the Russian Federation, are paid a monthly lifelong allowance;

- citizens discharged from military service or called up for military training who performed international duty in Afghanistan and other countries in which hostilities took place;

- individuals who received or suffered radiation sickness or became disabled as a result of tests, exercises and other work related to any types of nuclear installations, including nuclear weapons and space technology;

- parents and spouses of military personnel and government employees killed in the line of duty;

- individuals carrying out professional creative activities - in relation to specially equipped premises, structures used by them exclusively as creative workshops, ateliers, studios, as well as residential premises used to organize non-state museums, galleries, libraries open to the public - for the period such use;

- individuals - in relation to economic buildings or structures, the area of each of which does not exceed 50 m2 and which are located on land plots provided for personal subsidiary farming, dacha farming, vegetable gardening, horticulture or individual housing construction.

We recommend reading: Sample application to the court on a debt receipt

Property tax

Property tax is levied on residential buildings (cottages), dachas, garages, as well as other buildings and structures.

As in the previous case, the tax rate is determined by local governments, taking into account the relevant recommendations established by the Tax Code of the Russian Federation. In 2020, property tax rates are:

- 0.1% of the tax base of residential buildings and premises, as well as complexes that include residential premises, garages and other structures, household buildings with an area of no more than 50 sq.m. etc.;

- 0.5% of the tax base of other objects.

The established tax rates can be either reduced to zero or increased threefold by the same local authorities.

Legislation on the tax base

So which of the above is true and which is fiction? Firstly, we need to remember that the tax on country houses dates back to 1992. In order to find out the tax base, you need to refer to the legislation.

The object of taxation, according to the law on property tax for individuals, has remained virtually unchanged. Just as before, it is any real estate:

An important note made in Articles 1 and 2 of the law is that only owners pay this tax. Only those types of property that are registered in Rosreestr are considered property. Previously, the owner received a Certificate of Ownership after the registration procedure. Now - a legally equivalent extract from the Unified State Register of Real Estate.

In other words, only those buildings that can be registered in the state cadastre and obtain title to them are subject to tax. These can only be permanent buildings.

Capital buildings differ from temporary ones in that they have a strong foundation and long-term purposes for their use. There are several types of permanent buildings, but the main ones are residential and non-residential. All other buildings that present an unstable appearance and non-permanent purpose are classified as temporary.

Article 406 of the Tax Code of Russia (TC RF) supplements the tax base with the following objects:

- unfinished construction projects;

- a set of buildings that includes one or more residential buildings;

- outbuildings.

It remains to find out what kind of buildings we are talking about. Will grandparents really pay for every dilapidated building that is loudly called a greenhouse or barn? Representatives of the Ministry of Finance provide detailed explanations on this matter in the media.

How much residential or total area is taxed?

It is important for persons who own real estate to know about the nuances of accrual and exemption from taxes. The tax authorities are responsible for calculating the amount to be paid. But payers should check the calculations and notify the tax office of the existence of grounds for providing them with benefits.

We recommend reading: Repair on weekends in Bashkiria

What does it mean? When assessing housing by the specified dimensions, the cost according to the cadastre will be reduced. That is, if 1 sq. m. of the house is valued at 10,000 rubles, then the deduction from the total amount will be 50 * 10,000 = 50,000. And for a house with a total area of 80 square meters, the tax is taken into account only from 30. Nothing difficult.

What objects are taxed?

Infographics: tax on country houses in 2020

In February 2020, the Ministry of Finance on its official website published a response to numerous questions regarding the tax on summer cottages. From this explanation, we will try to find an exact answer to the question: what is taxed on a summer cottage and what is not.

At the beginning of its appeal, the Ministry of Finance identified many online materials on this topic as unreliable. It is further indicated that taxation on outbuildings on dacha and garden plots has existed since 1992. The Ministry of Finance is not going to introduce a new tax. So, the following buildings and outbuildings are taxed:

- Summer cuisine;

- bath;

- barn, outbuilding;

- Unfinished construction site.

There are many such objects in garden plots:

They are not subject to registration, which means they are not subject to taxation. This means that summer residents no longer have to worry about their, often dilapidated, buildings.

A very important note from the Ministry of Finance regarding their registration was that the owner of the site independently decides whether he needs to register his buildings. This applies not only to buildings. Until now, not all summer cottages have been registered as property by their owners. Only those who want to sell, donate or transfer property by inheritance take such a measure.

House area: total, built-up area and others

2. The total area of apartments should be determined as the sum of the areas of their premises, built-in wardrobes, as well as loggias, balconies, verandas, terraces and cold storage rooms, calculated with the following reduction factors: for loggias - 0.5, for balconies and terraces - 0.3 , for verandas and cold storerooms - 1.0. The area occupied by the stove is not included in the area of the premises. The area under the flight of internal stairs with a height from the floor to the bottom of the protruding structures is 1.6 m or more is included in the area of the premises where the stairs are located.

Garden house tax: studying the new tax code

- When calculating based on cadastral value, the tax rate for individuals cannot exceed 0.3%. Therefore, if the value of the property is 2 million per year, you will have to pay 2,000,000 x 0.003 = 6,000 rubles.

- But when calculating by inventory value, the maximum rate can reach 2%, which for the same two million rubles will already give 2,000,000 x 0.02 = 40,000 rubles.

We recommend reading: Can a husband sell his share in an apartment without his wife’s consent?

What buildings on a summer cottage are subject to tax in Russia?

- if a dacha plot is sold at the same or slightly lower price for which it was previously purchased, then the owner may be exempt from paying tax if he provides documentary evidence of the purchase and sale;

- if a dacha plot is sold at a slightly higher price and the owner has confirmation of this, then the amount of tax is deducted only from the difference between the sale and purchase price;

- if residential dacha properties are purchased, buyers may be provided with a tax deduction if its amount is equal to the value of the property and does not exceed 2 million rubles;

- the state is ready to provide a tax deduction even if the cost of the property being sold does not exceed 1 million rubles, which allows for a reduced amount of the tax base.

We recommend reading: Divorce with a mortgage and 2 children

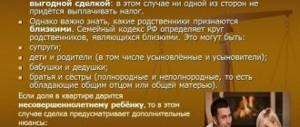

If a summer cottage plot is purchased under a purchase and sale agreement, then you will not need to pay tax upon purchase. But if the dacha becomes the property of a close relative under a gift agreement, then the recipient will have to pay personal income tax, the amount of which is calculated from the value of the donated dacha plot.