26.01.2019

| no comments

According to clause 3 of Article 38 of the Tax Code of the Russian Federation (2), any property sold or intended for sale is recognized as a commodity for tax purposes. Consequently, real estate intended for sale is recognized as a commodity for tax purposes and is subject to VAT in the generally established manner (Articles 146, 154, 164 of the Tax Code of the Russian Federation (2)) provided that the seller does not have benefits.

For real estate recorded in accounting accounts together with “input” VAT, a special procedure for calculating VAT upon its sale is provided (clause 3 of Article 154 of the Tax Code of the Russian Federation (2)). It can be:

- acquired premises used in carrying out transactions that are not subject to taxation (exempt from taxation);

- premises purchased using targeted budget funding and paid including VAT, which is not deductible, but is covered by other sources;

- premises received free of charge, accounted by the organization at a cost that includes the amount of tax paid by the transferring party.

When selling property that is subject to accounting at cost, taking into account the VAT paid (the tax was not reimbursed from the budget), the tax base is determined as the difference between the price of the property sold (determined taking into account the provisions of Article 40 of the Tax Code of the Russian Federation (2)), including VAT (without tax from sales), and the cost of the property being sold according to accounting data (residual value taking into account revaluations). According to clause 4 of Article 164 of the Tax Code of the Russian Federation (2), the tax rate is determined as a percentage of the tax rate of 18% to the tax base, taken as 100% and increased by the corresponding tax rate (in other words, the rate is 18/118) .

Reimbursement of “input” VAT from the buyer of the premises. If the purchasing organization is a VAT payer, then the tax paid to the seller is reimbursed from the budget in accordance with the generally established procedure on the basis of Articles 171 and 172 of the Tax Code of the Russian Federation (2). To do this, four conditions must be met:

- the premises were purchased to carry out transactions subject to VAT;

- the property has been paid for;

- there is a completed original invoice from the real estate seller;

- the premises are recorded in the accounting accounts.

An organization can fully deduct the VAT paid upon the purchase of real estate based on the seller’s invoice (Clause 1, Article 172 of the Tax Code of the Russian Federation (2)). Of course, if the acquired property is used in activities subject to VAT (clause 1, clause 2, article 171 of the Tax Code of the Russian Federation (2)).

The tax paid can be offset only after the fixed assets have been registered. This requirement is enshrined in clause 1 of Article 172 of the Tax Code of the Russian Federation (2). However, the Code does not say on which accounting account the acquired fixed assets should be reflected. Therefore, it is not clear whether for deduction it is enough to reflect the value of the object on account 08 “Investments in non-current assets” or whether it is necessary to wait for the fixed asset to be entered into account 01 “Fixed Assets”.

You can transfer real estate to account 01 only if you have documents confirming their state registration. This is provided for in clause 41 of Order of the Ministry of Finance of the Russian Federation No. 34n (27). And state registration of real estate will take at least a month. Therefore, if we consider the registration of a fixed asset to be reflected in account 01, then the moment of VAT deduction will be delayed.

In the meantime, the ambiguity of the wording of clause 1 of Article 172 of the Tax Code of the Russian Federation (2) gives rise to constant conflicts between taxpayers and “tax officers”. Thus, the latter believe that the tax paid can be deducted only after the property is registered as a fixed asset. According to the Chart of Accounts (25), fixed assets are accepted for accounting under account 01 “Fixed assets”.

Buying and selling real estate: all about taxes

However, the arguments of the “tax authorities” can be disputed. A fixed asset that has not yet been put into operation is the property of the organization. It has been accepted for accounting, but not on account 01, but for now on account 08. Even the Ministry of Finance says that real estate objects that have already been put into operation before the registration of ownership of them should be reflected on account 08 and even depreciation is charged on them ( Letter of the Ministry of Finance of the Russian Federation No. 16-00-14/121).

To deduct VAT, it does not matter in which accounting accounts the fixed asset is listed. The correctness of this position is confirmed by judicial practice. For example, the Federal Arbitration Court of the Moscow District also indicated that regardless of the fact that the fixed asset is reflected in account 08, VAT on it can already be deducted (Resolution dated July 22, 2002 in case No. KA-A40/5624-02).

If real estate was purchased for resale and accounted for in accounting on account 41 “Goods” or account 10-2 “Purchased semi-finished products and components, structures and parts,” then this is enough to reimburse the “input” VAT. However, when purchasing premises for the purpose of placing an office or production workshop in it, a necessary condition for the reimbursement of “input” VAT will be the registration of the property in account 01 “Fixed Assets”.

When purchasing unfinished objects that will subsequently be included in fixed assets, on the basis of clause 5 of Article 172 of the Tax Code of the Russian Federation (2), it is allowed to reimburse the “input” VAT paid to the seller only at the time of resale of the unfinished premises or after completion of construction in that month , when the organization first accrues depreciation on this object. By the way, if an organization purchased materials or hired contractors to complete construction, the “input” VAT paid to suppliers is also reimbursed after completion of construction at the time the first depreciation entries are reflected in tax accounting. For an object of depreciable property, depreciation is accrued from the 1st day of the month following the month in which the object was put into operation (Article 259 of the Tax Code of the Russian Federation (2)).

If an organization is going to buy an unfinished premises in order to complete it and resell it, and it is known in advance that the purchased property will be included in working capital, then in this case the general rules apply (fulfillment of the four conditions indicated above) for VAT refunds related to purchased inventory items. Moreover, if the premises are intended to be used for operations both subject to and not subject to VAT, the “input” VAT must be divided according to the rules given in paragraph 4 of Article 170 of the Tax Code of the Russian Federation (2) and distributed between the accounts for recording the cost of the premises and the reimbursement accounts VAT.

Income tax

The object of taxation when selling premises is the income received from the sale of real estate, reduced by the amount of expenses incurred (Article 247 of the Tax Code of the Russian Federation (2)). Income for the purposes of calculating profit tax is recognized for all large and medium-sized organizations using the accrual method based on Article 271 of the Tax Code of the Russian Federation (2). However, small organizations (with the exception of banks), in accordance with Article 273 of the Tax Code of the Russian Federation (2), have the right to determine the date of receipt of income (expenses) using the cash method, if the average amount of revenue from the sale of goods (work, services) over the previous four quarters ) of these organizations, excluding VAT and sales tax, did not exceed 1 million rubles. for each quarter when calculating tax.

The date of receipt of income is the date of transfer of ownership to the new owner upon sale of the premises, regardless of the time of payment (clause 3 of Article 271 and clause 1 of Article 39 of the Tax Code of the Russian Federation (2)). In Sect. 3 Methodological recommendations on income tax (48),

it is determined that the date of sale of goods is the day of transfer of ownership of goods, determined in accordance with the Civil Code of the Russian Federation (1).

Thus, the seller organization must reflect the proceeds from the sale of premises alienated on the basis of a purchase and sale agreement at the time of transfer of ownership to the new owner.

When selling real estate as an item of fixed assets at a loss, it cannot be written off at once and in full as a reduction in the tax base for the tax (reporting) period. To write off such a negative financial result, special rules are provided, given in paragraph 3 of Article 268 of the Tax Code of the Russian Federation (2). The resulting loss is included in the taxpayer's other expenses in equal shares over a period defined as the difference between the useful life of this property and the actual period of its operation until the moment of sale. Write-off of losses as expenses should begin in the month following the month in which the sale of the premises was made.

If the premises were purchased for resale, it does not qualify as depreciable property on the basis of Article 257 of the Tax Code of the Russian Federation (2). In this case, the loss from its sale on the basis of clause 2 of Article 268 of the Tax Code of the Russian Federation (2) simultaneously and in full reduces the tax base of the tax (reporting) period.

If real estate is purchased for resale and is included in non-depreciable property, depreciation is not charged on it.

According to Article 256 of the Tax Code of the Russian Federation (2), depreciable property includes assets that are owned by the taxpayer. The premises must be reflected in the tax registers only if the taxpayer-buyer of the building has registered ownership of it with the justice authorities.

For an object of depreciable property, depreciation is accrued for the purposes of calculating income tax on the basis of Article 259 of the Tax Code of the Russian Federation (2) from the 1st day of the month following the month in which this object was put into operation, and ceases from the 1st day of the month , following the month in which the implementation occurred. An order to put a property into operation for the purpose of calculating depreciation in accordance with Chapter 25 of the Tax Code of the Russian Federation (2) must be issued after state registration of ownership of the building.

Organizations purchasing used real estate objects have the right to determine the depreciation rate for this property taking into account the useful life reduced by the number of years (months) of operation of this property by the previous owners (Clause 12 of Article 259 of the Tax Code of the Russian Federation (2)).

If the period of actual use of the building by the previous owner turns out to be equal to or exceeds its useful life, determined in accordance with the Decree of the Government of the Russian Federation No. 1 (21), the taxpayer has the right to independently determine (issue an internal order) the useful life of this property, taking into account safety requirements and other factors.

Based on clause 1 of Art. 257 of the Tax Code of the Russian Federation (2) the taxpayer cannot change the initial cost of fixed assets when calculating depreciation for tax purposes as a result of revaluations. If revaluation is nevertheless carried out, it is necessary to calculate depreciation separately for tax and accounting purposes.

Depreciation in tax accounting can be calculated using linear and non-linear methods, but for buildings falling into groups 8, 9 and 10 ( RF Government Decree No. 1 (21

)), an exception has been made.

For them, depreciation can only be calculated using the linear method based on clause 3 of Article 259 of the Tax Code of the Russian Federation (2). Moreover, for accounting purposes, organizations have the right to use useful lives to calculate depreciation on the basis of the specified resolution. However, if fixed assets were acquired before January 1, 2002, depreciation on them for accounting purposes is calculated on the basis of useful lives, also adopted before 2002 (most organizations used useful lives based on the “Unified Depreciation Standards” (20 )

).

Payment for land.

According to paragraph 1 of Art. 552 of the Civil Code of the Russian Federation, part II (1), under a contract for the sale of premises, the buyer, simultaneously with the transfer of ownership of the real estate, is transferred the rights to that part of the land plot that is occupied by this real estate and is necessary for its use.

According to Art. 16 Law of the Russian Federation “On payment for land” (15)

for land plots intended for servicing buildings that are in the separate use of several legal entities or citizens, land tax is calculated separately for each in proportion to the area of the building that is in their separate use.

In addition, in accordance with clause 1 of Article 35 of the Land Code of the Russian Federation (3), when the ownership of real estate is transferred to another person, the new owner acquires the right to use the corresponding part of the land plot occupied by this building (structure, structure) and necessary for its use on the same terms and to the same extent as the previous owner.

Thus, if the transfer of ownership of real estate under real estate purchase and sale contracts is registered, then the land tax from the buyer of the building must be calculated starting from the month following the month of registration of the transfer of ownership of real estate on the basis of Art. 17 Law of the Russian Federation “On payment for land” (15)

, regardless of the time of receipt of the document certifying ownership of the land plot. Until this time, the payer of land tax is the seller of the building.

In accordance with the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated January 09, 2002 No. 7486/01

The absence of a document on the right to use land, the receipt of which depends solely on the will of the land user himself, cannot serve as a basis for exempting him from paying land tax.

Issues of making rent payments for land are regulated in the same manner. You must immediately contact, for example, Moskomzem and renew the land lease agreement. Otherwise, Moskomzem can legally recover rent from the new owner of the property on the basis of Article 552 of the Civil Code of the Russian Federation, Part II (1), which is confirmed by judicial practice (Resolution of the Federal Antimonopoly Service of the Moscow District dated June 28, 2002 No. KG-A40/4013-02 ).

Property tax.

According to Chapter 30 “Property Tax of Organizations” of the Tax Code of the Russian Federation (2), the tax base includes the value of property recorded on the balance sheet as fixed assets in accordance with the established accounting procedure (clause 1 of Article 374, clause 1 of Art. 375 Tax Code of the Russian Federation (2)). Obviously, in order to save on property tax, it is more profitable for an organization to take into account real estate, ownership rights for which have not undergone state registration, in account 08. In this case, according to the code, a significant value of real estate is not subject to taxation.

Specialists of the Ministry of Taxes of Russia believe that the value of property, the documents for which have been submitted for state registration and which is actually in use, should be taken into account in account 01 and subject to property tax.

But property tax under Chapter 30 of the Tax Code of the Russian Federation (2) is paid on real estate recorded “on the balance sheet as fixed assets in accordance with the established accounting procedure” (clause 1 of Article 374 of the Tax Code of the Russian Federation (2)), and not according to the instructions of the “tax authorities”.

But if an organization takes into account real estate, without waiting for state registration, on account 01, then it will definitely not have problems with deducting VAT. After all, the “tax authorities” believe that this tax can be deducted only after the transfer of fixed assets to account 01 (clause 1 of Article 172 of the Tax Code of the Russian Federation (2)).

Therefore, when choosing an accounting option for unregistered real estate, an organization needs to decide what is more profitable for it: not to pay property tax before state registration or, rather, to offset VAT. But if real estate is purchased without VAT or is paid only after registration, then it is clear that it is better to account for the property in account 08 and not pay tax on it.

Is the sale of apartments subject to VAT?

In fact, VAT is a value added tax that is charged to the buyer. VAT is added up at all stages of production of goods and includes all additional costs incurred by the manufacturer. This amount must be paid earlier than the final cost of the goods in the order in which expenses arise; in fact, of course, this amount is simply included in the total cost of the goods. However, there is a list of property that is not subject to VAT. Is the sale of apartments subject to VAT ? No, this property is included in the list of precisely those properties that are not subject to value added tax, regardless of who the buyer and seller are in terms of property.

An organization sells an apartment to an individual: accounting and taxation

Important

Alexey Slesarev wrote: And these are the requirements of the Central Bank and the RFA. The head of the organization is obliged to know this. Just in case, I'll clarify. The legal entity is a resident of the Russian Federation, the seller will probably also be a resident, payment is in rubles, is a transaction passport still needed? Asti495 wrote: For what purpose? Can you imagine the volume of taxes and the features of accounting on the balance sheet? And if you need to sell, do you understand how much this pleasure will cost? The office wants to help me with an apartment, namely: buy it for myself, and then resell it to me for the same price when I have enough funds.

If I understand correctly there will be a property tax of 2%. I can’t imagine the specifics of accounting. And, judging by your comments, during the resale there will be some large costs for me? PS

Sale or purchase of an apartment by a legal entity

The Tax Code provides for different forms of tax implementation for legal entities and individuals, but payment of VAT when selling or buying an apartment is always the same. This type of purchase or sale is not subject to VAT. Real estate is a separate form that is subject to personal income tax only, regardless of whether you buy/sell it to a legal entity or an individual.

Example:

For example, a legal entity decided to purchase 5 apartments during the construction phase for further sale; the legal entity itself is engaged in other activities, but decided to make money on it. When concluding an agreement between a legal entity and a construction organization, the amount of the agreement was 6,250,000 rubles. In fact, only this amount was paid to the developer. A year later, the construction organization issued certificates for 5 to the founder of the legal entity for whom the contract was drawn up. After selling these 5 apartments at a price of 2,000,000 rubles, the legal entity receives a final income of 10,000,000 rubles, which is also the final amount that the seller receives. In this case, only 13% personal income tax is paid, and VAT in the amount accepted in our country of 18% is not paid by either party.

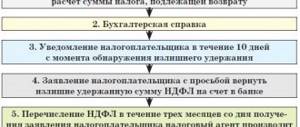

Personal income tax refund - the last word belongs to the taxpayer

- The purchased real estate is located in Russia;

- An individual purchasing housing regularly pays income tax of 13 percent;

- The housing was purchased at the expense of the taxpayer himself. Housing purchased with maternity capital, budget funds with state funding or at the expense of an enterprise is not taken into account;

- The purchase and sale agreement was concluded between people who are not relatives, as well as subordinates;

- Expenses do not exceed 2 million rubles.

We recommend reading: Can I apply for alimony if we are married and live together?

VAT refund when purchasing an expensive asset is easier to do through an entrepreneur

VAT refund when purchasing an expensive asset is easier to do through an entrepreneur

How can a company in a special regime recover VAT when purchasing an expensive property?

There is no need to restore tax upon termination of the activities of an individual entrepreneur.

What is the most profitable way to transfer an object from an entrepreneur to a company?

VAT reimbursement when purchasing expensive property is almost always associated with an in-depth desk audit (clause 8 p. 89 of the Tax Code of the Russian Federation). Tax officials cling to every little thing to refuse a tax refund. To avoid this, the purchase of the object is registered in the name of the entrepreneur, who will then transfer the asset to the company.

The same option is suitable for the purchase of a fixed asset by a “simplified” or “imputed” person. In general, a company in a special regime does not have the right to a VAT refund, since it is not a payer of this tax (clause 2 of article 346.11, clause 4 of article 346.26 of the Tax Code of the Russian Federation). Using a friendly entrepreneur in the general mode will allow you not to lose on taxes.

Savings are based on the entrepreneur’s right to refund VAT

The essence of the optimization method, which is used in practice, is as follows (see diagram on page ##). To purchase a fixed asset, the company attracts a friendly individual, who registers as an individual entrepreneur under the general taxation regime. After purchasing an asset, the entrepreneur submits a VAT refund. Since individual entrepreneurs have few transactions, tax refunds usually occur without any problems. After some time, he ceases his activities, having in his possession a liquid asset and the amount of refunded VAT in his current account. The further transfer of the asset to the company depends on its tax treatment and the needs of the parties. In particular, the transaction can be formalized in the form of a purchase and sale, a contribution to the authorized capital or a gratuitous transfer.

Scheme

How an entrepreneur can help recover VAT when purchasing expensive property

In the absence of violations, the period for making a decision on VAT refund may be about 3.5 months from the date of filing the declaration. This deadline must be observed, unless, of course, the tax office decides to refuse compensation on far-fetched grounds, which also cannot be ruled out. In particular, you will need:

— 3 months — for a desk audit (clause 2 of Article 88 of the Tax Code of the Russian Federation);

— 7 working days — for the inspection to make a decision (clause 2 of Article 176 of the Tax Code of the Russian Federation);

— 5 working days — transfer of funds to the taxpayer’s account (clause 8 of Article 176 of the Tax Code of the Russian Federation).

It is important that in order to receive tax reimbursement, the acquired asset must be used in activities subject to VAT. For example, it can be rented out, even for a short time. Moreover, the tenant may be the main company itself, to which the property is intended.

If an entrepreneur does not have VAT to accrue at all, then he will face an almost guaranteed refusal to receive a refund. Of course, one can argue that all the conditions of the Tax Code of the Russian Federation for submitting a deduction are met. That the established arbitration practice proceeds from the fact that the right to deduction does not depend on the presence or absence of transactions subject to VAT in the disputed period (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 05/03/06 No. 14996/05). But all this will only create problems, which the company planned to get rid of by resorting to the services of an entrepreneur.

As for the source of financing for the purchase of an asset, there are several options. If an individual plans to become a co-founder in the main company in the future, then he can purchase an object at his own expense, and then contribute it to the authorized capital of the company.

Another option is that the object is paid for from borrowed funds received from a friendly company, and the debt is repaid from the funds received from the sale of the object. Note that tax authorities can revive the old position, according to which VAT on a purchase paid with borrowed funds is not reimbursed, since the company did not incur real costs (determination of the Constitutional Court of the Russian Federation dated April 8, 2004 No. 169-O). Officials have long abandoned this opinion (letters from the Ministry of Finance of Russia dated July 27, 2006 No. 03-04-11/128, dated August 31, 2005 No. 03-04-08/228), but local inspectors can use this reason for a far-fetched refusal. Therefore, in practice it is usually formatted this way. An individual receives financing to a personal account, without recording the individual entrepreneur, and then finances the purchase of the object from his own funds. Thus, the accounting will not show that the funds were borrowed.

There is a simplified procedure for terminating the activities of an entrepreneur

So that when transferring an asset to a company, the entrepreneur does not incur VAT, by this time he ceases his activities and further acts as an ordinary individual. To do this, the entrepreneur must submit the following documents to the registration authority: an application, a receipt for payment of the state duty, as well as a document confirming the submission of the necessary information to the territorial body of the Pension Fund of Russia (Article 22.3 of the Federal Law of 08.08.01 No. 129-FZ). Within five days from the date of submission of documents, the registering authority must complete the registration of the loss of the corresponding status (clause 8 of article 22.3, clause 1 of article 8 of Law No. 129-FZ).

Let us note that, unlike an organization (Article 89 of the Tax Code of the Russian Federation), in relation to an entrepreneur, the Tax Code of the Russian Federation does not require an on-site inspection to be carried out upon termination of its activities. There is also no obligation to submit a message to the inspectorate about the loss of individual entrepreneur status, because this rule is applicable only for cases of liquidation of organizations (Clause 2 of Article 23 of the Tax Code of the Russian Federation). Thus, the possibility of conducting an on-site tax audit is unlikely, although not excluded.

After the official termination of business activities, an individual is not required to keep documents confirming receipt of income. This rule applies only to organizations and individual entrepreneurs (subclause 8, clause 1, article 23 of the Tax Code of the Russian Federation). Therefore, even if inspectors subsequently request documents, for example, for a counter check with the buyer (Article 93.1 of the Tax Code of the Russian Federation), the citizen may not present them. It is quite possible that this will have to be proven, so in order to avoid a dispute, it is still better to save the documents.

The Code does not oblige an entrepreneur to restore VAT upon termination of activity

The entrepreneur does not face any negative tax consequences when terminating his activities. Perhaps the only trouble may be the tax authorities’ demand to restore the amount of VAT on an object acquired for business activities and remaining in the ownership of a citizen. The inspectors' arguments boil down to the fact that in this case the property is not used for operations subject to VAT, and this is the basis for the restoration of the tax by virtue of subparagraph 2 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation.

Of course, such demands are unlawful. This provision of the Tax Code is applicable only if the taxpayer continues to conduct his business activities, but for various reasons loses the status of a VAT payer. For example, when switching to a simplified taxation system (clauses 2, 3 of Article 346.11 of the Tax Code of the Russian Federation). Or after receiving exemption from the duties of a taxpayer (Article 145 of the Tax Code of the Russian Federation).

In addition, paragraph 3 of Article 170 of the Tax Code of the Russian Federation contains a closed list of circumstances in which the taxpayer is obliged to restore the VAT previously accepted for deduction.