In this article we will look at the tax deduction when exchanging an apartment. Let's learn about the registration procedure. We will sort out the necessary documents.

When carrying out a housing exchange transaction, as well as when concluding a purchase and sale agreement, the buyer and seller have tax obligations. The exchange agreement is also the basis for obtaining a property deduction for each of the parties to the agreement. Today we will talk about the specifics of filing a deduction under an exchange agreement, and also provide answers to common questions on the topic.

Tax obligations when exchanging housing

Under the provisions of the Tax Code, the party that exchanged real estate on the basis of an exchange agreement is required to pay personal income tax only if the exchange was made with an additional payment. The grounds for taxation are as follows: the amount of funds in the form of an additional payment is recognized as income on which tax must be paid, that is, the taxpayer is recognized as the person whose apartment was valued at a lower value upon exchange.

If the parties exchanged apartments of equal value, then there is no need to pay tax. The same rule applies to any real estate that, within the framework of the contract, was recognized as equal in price. That is, half a house can be exchanged for an apartment, a room for a country house, etc. If the agreement does not stipulate the fact of additional payment, then the parties do not have obligations to pay tax.

Do I need to pay tax when exchanging an apartment?

The Tax Code does not provide for separate conditions for paying taxes for exchange agreements. The Civil Code also does not detail the concept. But in one of the articles you can find a mention that the exchange is equivalent to a standard purchase and sale transaction.

If there was an additional payment, then it is possible to submit documents for a tax deduction. There are no restrictions on the amount of additional payment, so you can get the full amount. If housing is transferred between relatives, the Tax Inspectorate may refuse to pay the deduction.

Exchange of an apartment with an additional payment: is it possible to get a deduction?

What is the situation with barter contracts, the provisions of which provide for additional payment? The person who received the additional payment is burdened with tax obligations. But at the same time, each of the parties to such an agreement acquires the right to receive a property deduction, which means that the amount of tax can be reduced, and in certain situations, its payment can be avoided altogether.

Let's start with the person who is initially exempt from paying the tax. A citizen who, as a result of an exchange agreement, became the owner of more expensive housing (that is, the one who made the additional payment) in this case does not acquire tax obligations, but can receive a refund of the amount by filing a deduction. Unlike the general procedure, when compensation is calculated based on the cost of housing, the amount of return under an exchange agreement is calculated from the amount of the additional payment.

Example No. 1.

Kupriyanov S.D. entered into an exchange agreement, within the framework of which he sold his own room (estimated value - 981,405 rubles) and purchased an apartment (estimated value - 1,604,880 rubles). For the amount of the additional payment, Kupriyanov issued a tax refund in the amount of 81,051.75 rubles. ((RUB 1,604,880 – RUB 981,405) * 13%).

Deduction for the amount of additional payment received

Now let's look at the taxes that must be paid by the person who received the surcharge. According to the Tax Code, the entire amount of the additional payment is recognized as income, which means that the taxpayer should transfer 13% of the funds received to the budget. But at the moment the object of taxation (income) arises, the citizen has the right to receive a tax deduction in the amount of 1 million rubles. The tax payable is calculated from the difference between the amount of the surcharge and the deduction:

N = (Add – Sub) * 13%,

where N is the tax payable;

Additional payment – income received by a citizen when exchanging housing (surcharge);

Deduction – fixed amount of 1 million rubles.

Thus, the person who made the exchange has a real chance to be freed from the tax burden: if the amount of the additional payment received is less than or equal to 1 million, there is no need to pay income tax.

Example No. 2.

Skvortsov exchanged a country house (estimated value - 2 million 420 thousand rubles) for a two-room apartment (estimated value - 1 million 806 thousand rubles) and received an additional payment of 614 thousand rubles. Since the tax base (614 thousand) is less than the deduction, Skvortsov does not need to pay tax.

Another way to reduce the tax burden or exempt from paying tax completely is to apply for a deduction for the amount of the purchase of housing. In this case, the following mechanism is provided: if the person who received the additional payment has documents confirming the expenses for the sold housing, then the citizen can reduce the tax base by the amount of such expenses. If the apartment is sold for less than the purchase price, then you do not need to pay tax.

If the apartment has been owned for more than 3 years / 5 years

Let's say you sold an apartment in exchange and received an additional payment, but none of the above deductions completely exempts you from paying taxes. What other ways can you reduce your tax base? According to the Tax Code, owners who have sold housing registered by the owner for more than 5 years are given the right to use a deduction in the amount of 100% of the amount of income received. This rule applies to housing sold under an exchange agreement after 01/01/16. For apartments that were exchanged before the specified period, more favorable rules apply. To be exempt from taxes, the owner who exchanged housing and received income must own the housing for at least 3 years before the exchange.

The right to receive a deduction

The tax rate when drawing up an agreement for the exchange of an apartment will be the same as when selling property. Therefore, the right to receive a tax deduction will be the same.

Conditions

If you follow the law, the following property deductions are possible:

- In the amount of expenses for purchasing housing under an exchange agreement (no more than 2,000,000 rubles).

- In the amount of income from the alienation of residential premises under an exchange transaction (not more than 1,000,000 rubles).

To qualify for the benefit, you must be a tax resident of the Russian Federation and, in addition, receive income that is subject to taxation at a rate of 13%.

Procedure

To receive a deduction, you must contact the Federal Tax Service at the end of the calendar year (at the beginning of the next year after the exchange transaction was executed). To do this, the tax inspector at the place of registration is provided with:

- statement;

- personal income tax declaration form 3 (can be filled out at the Tax Inspectorate when submitting an application);

- Form 2 of personal income tax – certificates from places of employment about income received, deductions (information for the previous year);

- photocopies of documents confirming the fact of the transaction;

- details of the account to which the deduction will be transferred.

You can submit documents:

- Personally. The advantage is that they will immediately check the correctness of filling. This will reduce the time required for returns and rework.

- By mail. Sent by registered mail with a description of the attachment. Copies must be notarized.

From the date of filing the application, the refund must be paid within 1 month. The law provides for an additional period of 3 months for verification of submitted documents, so you can receive the required amount into your account later.

If the deduction is denied, a notice is sent indicating the reasons.

It will also be possible to receive a tax deduction later from the employer, simply indicating in the application that it is planned to be taken into account as subsequent deductions. Then no salary tax will be collected for some time until the due amount is compensated.

We process compensation: procedure and documents

Registration of deductions when exchanging housing is carried out in the general manner. Before starting the procedure, prepare the following documents:

- barter agreement;

- act of acceptance and transfer of housing;

- payment documents (receipt for additional payment, receipt, bank statement);

- 2-NDFL certificate received from the employer indicating the amount of tax paid for the period;

- an extract from Rosreestr on the ownership of the purchased housing;

- declaration 3-NDFL (if the deduction is issued through the Federal Tax Service);

- application (in the form established by the employer or the Federal Tax Service - depending on the method of registration);

- ID cards (original and copy of passport);

- real estate purchase and sale agreement (if the deduction is issued for the amount of expenses incurred for the purchase of housing);

- an extract from Rosreestr for the sold apartment, confirming the period of ownership of the housing (if an exemption from paying tax is issued for real estate owned for more than 3/5 years).

If you are officially employed, then it is advisable for you to file a deduction through your employer. Documents should be submitted to the accounting department at the place of duty immediately after the transaction has been completed and all documents have been collected. When applying for compensation in this way, you will not need to order a 2-NDFL certificate and prepare a tax return. 10 days after submitting the papers, you will be assigned a deduction. You will be paid compensation in the amount of 13% of your salary every month until the entire refund amount is exhausted. If you submitted documents later than the exchange period (the apartment was sold in February, and the documents were transferred in November), then you will be recalculated the tax for the period from the moment the transaction was completed until the day the documents were submitted. The recalculation amount will be paid to your card account.

If you are a non-working pensioner or registered as an individual entrepreneur, then you should submit documents for a refund through the Federal Tax Service. The deadline for submitting papers and declarations is April 30 of the year following the year of the exchange. With this registration method, compensation will be paid in the total amount to the details specified in the application.

What do government representatives think about the barter agreement?

The simplest opinion for the people was the motivation of the Russian Ministry of Finance. It was reflected in some legislative acts. According to this opinion, an exchange agreement is the same as a purchase and sale agreement, where each party is a seller and a buyer. When real estate has been owned by a person for more than three years, it is not subject to tax upon sale.

Representatives of the tax service see the whole situation in their own way. Based on their opinion, it becomes clear that when exchanging an apartment, a person does not spend his own funds, except in cases where an additional payment needs to be made. Therefore, the tax should be calculated only on the amount of payment made, and the right to a tax deduction should not apply to the exchange agreement.

Judicial practice shows that sometimes people go to court with controversial issues regarding taxation under an exchange agreement.

Especially for such cases, it is established that a person can receive income:

- in monetary terms;

- in material form;

- in kind.

In the first two cases, no problems arise, but when it comes to income in kind, sometimes misunderstandings occur. Especially for this, the judges clarified that if one apartment under an exchange agreement is completely equal in value to another apartment, then such a transaction should not be burdened with tax.

Do I need to pay?

The tax service does not particularly carefully check the payment of taxes when registering civil transactions.

Don't underestimate this. There is always a possibility that in the future, when registering new transactions with this real estate, a situation with tax evasion will arise.

The fine in such a situation will be many times higher than the insignificant amount of tax.

When can you not do this?

Provided that a free and equivalent transaction is carried out between persons having citizenship of the Russian Federation, taxes can be avoided. This leniency does not apply to foreigners or non-residents of the country. The tax fee will not be charged when exchanging real estate that has been owned for more than 3 years .

What to do if the property has been owned for less than 3 years?

Let's figure out whether tax is paid during such an exchange of an apartment. The amount of tax depends on such factors as ownership of real estate for up to 3 years. When concluding an agreement for the exchange of living space that has been owned for less than 3 years, the tax amount will be 13%. It is worth considering that taxes are assessed on an amount that exceeds 1 million rubles.

Documents attached to the declaration

To submit 3-NDFL after the sale of real estate that was owned by ownership, a citizen must attach other documents.

Such documents may include:

- A copy of the real estate purchase and sale agreement, which indicates the cost of housing;

- A receipt or other document establishing the receipt of funds, including a bank account statement.

To receive a personal income tax calculation under the “income minus expenses” program, you must attach:

- An old contract that establishes the rights of possession and disposal of the applicant;

- Documents of ownership – extract from the Unified State Register of Real Estate;

- A settlement document establishing the amount of expenses incurred by a citizen, including a receipt from the former owner, a statement from the bank about the transaction performed, or a check for replenishing the account of another person.

- A copy of your passport and other documents that Federal Tax Service employees may require.

An example of filling out 3-NDFL will help reduce the time required to record all information. When selling housing and filling out a declaration, the income code is indicated by the number “01”. Further, if there is a need to issue a deduction, fill in the relevant data indicating additional attachments to confirm the circumstances of the purchase.

Filling out 3-NDFL when selling an apartment is a lengthy process that can be shortened significantly by filling out online forms on the Federal Tax Service website indicating the relevant circumstances.

Taxes on barter transactions and how to reduce them

Tags: Apartments for sale, Taxes

We have already written about barter transactions, when one property is exchanged for another. Today we will talk about the tax on income arising from the exchange of real estate.

After all, under an exchange agreement, property is sold on the one hand, and acquired on the other, and this must be taken into account when calculating the tax.

Often this calculation raises questions - we decided to clarify them with the help of the notary of the Notary Chamber of St. Petersburg, Alexey Komarov.

Before or after the Tax Code changes?

When calculating the tax base, i.e. the amount from which the tax is calculated, first of all, you need to know when the ownership of the exchanged property arose: before or after January 1, 2020, i.e. before or after the changes came into force to the Tax Code, introduced by Federal Law of November 29, 2014 N 382-FZ.

If the exchanged object was acquired before January 1, 2020 (and the general rule states that ownership arises from the moment of state registration, except in cases of receipt of real estate by inheritance and acquisition under a share accumulation agreement, i.e. through a housing cooperative), then for the exchanger it is valid grace period of 3 years, regardless of the basis for acquiring this object. After this period, in the event of the sale of real estate, he is exempt from tax in principle and does not even file a declaration in this regard.

If the alienated apartment was acquired by the exchanger already in 2020, then in order to determine the minimum maximum (preferential) period of ownership of real estate, after which the tax is not paid and a declaration is not filed, the already amended Tax Code distinguishes between the grounds for the acquisition of real estate being sold or exchanged.

If the exchanger received the exchanged real estate as a result of inheritance or under a gift agreement from a family member or close relative, under an annuity agreement - lifelong maintenance with a dependent or through privatization, then the old grace period is valid - three years, after which when selling the object for any value no tax is paid.

For other grounds for acquisition, a five-year period of ownership of real estate is established. So, for example, if you bought the exchanged property after January 1, 2020, then in order to sell the apartment for any value without paying income tax, you will need to wait five years from the date of purchase.

How to calculate the tax base

If you have owned the real estate that you are alienating under an exchange agreement for less than a grace period, then you need to determine the income that you received as a result of the sale of real estate and the tax base.

To determine these values, the date of acquisition of the alienated real estate into ownership is precisely important. If the property was registered before January 1, 2020, then the amount specified in the contract is used to calculate income.

For example, if the value of an object under an exchange agreement is 3 million rubles, then the income received will be equal to 3 million rubles, and a 13% tax will be calculated on this amount.

If the property was registered after January 1, 2020, then the cadastral value of the property is used to calculate the tax, taking into account the correction factor.

For example, if under an exchange agreement the value of an object is 2 million rubles, and the cadastral value is 4 million, then the income received is calculated as follows: 4 million must be multiplied by an adjustment factor of 0.7, resulting in 2.8 million rubles.

Thus, the cadastral value, taking into account the coefficient, will be 2.8 million rubles, this amount is greater than the amount of the contract, so the income will be calculated precisely from this amount, and not from the value specified in the exchange agreement.

If, according to the contract, the cost of the object is 3 million rubles, and the cadastral value, multiplied by 0.7, is 1.5 million rubles, then 3 million rubles must be taken as the income received.

Two ways to reduce tax

However, a money changer who has income subject to taxation has the right to reduce the tax base, but only according to one of two schemes:

1) “income minus deduction” or

2) “income minus expenses.”

Using the “income minus deduction” scheme, you can reduce your income by a property tax deduction in the amount of 1 million rubles. For example, if one owner changes a house and land and is not exempt from taxation for the preferential period of ownership of real estate (see.

above), and the cost of a house is, say, 3 million rubles, land - 1 million rubles, then the income tax is calculated as follows: ((3 million + 1 million) - 1 million deduction) * 13% = 390 thousand rubles .

When using the 1 million deduction, remember that it is applied once per tax period, i.e. per year.

Using the “income minus expenses” scheme, you can reduce income by subtracting from it the expenses for the exchanged property. Let's use the same example with a house and land.

You can reduce the tax base, for example, by the cost of buying a house 2 million rubles, the cost of buying land 500 thousand rubles.

All that remains is to calculate the tax: ((3 million + 1 million) – 2 million cost of buying a house – 500 thousand cost of buying land) * 13% = 195 thousand rubles.

But not all expenses can be taken into account.

For example, if a house was purchased without specifying the lack of finishing in the contract, then it will not be possible to reduce income by the amount of finishing.

It is interesting that, according to the Letter from the Federal Tax Service, the costs of purchasing sanitary equipment, namely: bathtubs, plumbing fixtures, gas stoves, water and electricity meters, are not included in the above list of expenses. Of course, if it is possible to confirm expenses, then it is often more profitable to use the “income minus expenses” scheme.

By exchanging real estate under an exchange agreement, each party to the agreement also acquires housing.

Accordingly, in addition to one of the above schemes, the taxpayer can also use a property deduction when purchasing 2 million rubles, unless, of course, the amount has not been exhausted before, since it is provided only once in a lifetime.

And then the tax calculation in the example of a house and land in the prism of the “income minus deduction” scheme will look like this: ((3 million +1 million) - 1 million deduction on sale - 2 million deduction on purchase) * 13% = 130 thousand . rubles.

https://www.youtube.com/watch?v=IT8O94qeTLU

By using all legal possibilities to reduce the tax base, you can significantly reduce the amount of tax.

“I would like to emphasize the importance of explanatory letters from the Ministry of Finance and the tax inspectorate on the rules for applying this or that deduction,” adds notary Alexey Komarov.

“It would also be useful to consult with a notary or a specialist involved in taxation for the correct structuring of the exchange agreement that you are going to conclude, and in order to resolve controversial issues before concluding an exchange transaction, it is worth sending an official request to the tax office at the place of filing the tax return.”

Read more about barter transactions here.

Source: https://www.mirkvartir.ru/journal/analytics/2016/11/28/nalogi-pri-sdelkah-meni-i-kak-ih-ymen_sit/

Municipal housing

If citizens live in an apartment on the basis of a social tenancy agreement, then they also have the right to exchange the living space for an equivalent one. To do this you need:

- find a similar apartment;

- obtain permission from the municipal authority;

- obtain the consent of all tenants.

It is not allowed to exchange municipal real estate for private property, as well as for larger or smaller living space. For example, you cannot exchange a three-room apartment for a one-room apartment, since such a transaction is unequal and involves additional payments in favor of one of the parties.

The state is recognized as the owner of municipal housing, therefore, when alienating/receiving an apartment owned by a citizen on the basis of a social tenancy agreement, the obligation to pay personal income tax does not arise.

What amount is tax paid on?

Now the personal income tax on the sale of housing is calculated not only from the actual profit received, but also taking into account the cadastral value of real estate. If circumstances arise that confirm the sale of a home at a price lower than its market value and less than 70% of the cadastral value, a coefficient of 0.7 is used to calculate the citizen’s obligations, which is multiplied by the cadastral value of the subject of the contract.

When selling housing, the sale of which brings a profit of more than one million rubles, you will have to pay a tax at a rate of 13%. This type of tax burden is recognized as a personal income tax and is subject to declaration, so it is necessary to both report to the tax office and pay a certain amount of taxes before the time established by law.

Within the framework of Art. 224 of the Tax Code of the Russian Federation, the tax on the sale of an apartment by a non-resident of Russia is 30% of the amount received by the seller. Residents of the Russian Federation are persons living in the territory of the state for 183 days over the past 12 months.

Tax payment terms

Income received from the sale or exchange of property that has been in your possession for a long time is not subject to tax. Long term is considered:

- if the apartment was acquired before 2020 - 3 years or more. 3 years is 36 consecutive months;

- if the apartment was acquired in 2020 or later (for example, in 2020 or 2020) - 5 years or more. 5 years is 60 consecutive months.

There are exceptions to this rule. The 3-year period also applies to apartments that were received:

- by inheritance;

- as a gift from a close relative (for information on who exactly is considered a close relative, see Article 14 of the Family Code);

- under privatization or rent agreement.

Thus, 2 dates are important to you:

- the first is to obtain ownership of the apartment;

- the second is the registration of ownership of your apartment to the new owner.

To avoid paying tax, the difference between these dates must be 36 or 60 months or more.

Duration of ownership of the exchanged apartment

| How and when did you get the apartment? | A tenure that allows you to avoid paying taxes |

| Received before 2020 | 3 years (36 months) |

| Inherited (in any year) | 3 years (36 months) |

| Received as a gift from a close relative (in any year) | 3 years (36 months) |

| Received through privatization (in any year) | 3 years (36 months) |

| Received under an annuity agreement (in any year) | 3 years (36 months) |

| Purchased in 2020 and later | 5 years (60 months) |

| Received under preschool education in 2020 and later | 5 years (60 months) |

| Received under an exchange agreement in 2020 and later | 5 years (60 months) |

| Received as a gift from a non-relative in 2020 or later | 5 years (60 months) |

In most cases, ownership of real estate arises at the time of its state registration and entry into the state register of rights to real estate and transactions with it. You can find the date of such registration:

- in the certificate of ownership (if any);

- in an extract from the state register of real estate rights (it can be obtained from the MFC at the location of the apartment).

This rule applies to apartments:

- purchased under a purchase and sale agreement;

- received in exchange under a barter agreement;

- received from local administrations in connection with the demolition of dilapidated housing;

- received through privatization;

- received under DDU (equity participation agreement in construction).

There are exceptions to this rule. They relate to inheritance (the apartment is considered owned from the date of death of the testator) and real estate received in a cooperative (the apartment is considered to be owned from the day the share is paid in full). In these situations, the date of state registration of property is not important.

Let us emphasize again. The 3-year rule applies to apartments:

- received ownership before 2020;

- received by inheritance, as a gift from a close relative, through privatization or an annuity agreement.

So, if the apartment that was transferred in exchange was in your ownership for 3 years or more (36 months or more), then the income received from the exchange is not taxed. There is no need to declare it. Accordingly, for transactions with such real estate there is no need to pay tax or file a tax return.

Example: An apartment was inherited in September 2020. It is transferred to another person (buyer) under an exchange agreement.

Situation 1The ownership of an apartment transferred under an exchange agreement was registered to another person (buyer) in December 2022. In this case, the total period of ownership of the apartment will be 39 months (from September 2020 to December 2022).

In this situation, you do not need to pay income tax or file a return on it.

Situation 2The ownership of an apartment transferred under an exchange agreement was registered to another person (buyer) in April 2022. In this case, the total period of ownership of the apartment will be 28 months (from September 2020 to April 2022).

In this situation, you must declare income and submit a return. The obligation to pay tax depends on the amount of income received.

If the apartment that was transferred in exchange was purchased in 2016 or later and at the time of exchange was in your ownership for 5 years or more (60 months or more), then the income received from the exchange is not taxed. There is no need to declare it. For transactions with such real estate, you do not need to pay tax or file a tax return.

We suggest you read: What documents will be required to inherit an apartment?

ExampleThe apartment was purchased in March 2020. It is transferred to another person (buyer) under an exchange agreement.

Situation 1The ownership of an apartment transferred under an exchange agreement was registered to another person (buyer) in May 2024. In this case, the total period of ownership of the apartment will be 62 months (from March 2020 to May 2024).

Situation 2The ownership of an apartment transferred under an exchange agreement was registered to another person (buyer) in February 2024. In this case, the total period of ownership of the apartment will be 59 months (from March 2020 to February 2024).

The Tax Code does not provide for separate conditions for paying taxes for exchange agreements. The Civil Code also does not detail the concept. But in one of the articles you can find a mention that the exchange is equivalent to a standard purchase and sale transaction.

It is legally determined that if the property was purchased before 2020, then the tax is paid when it was owned for less than 3 years. But if you purchased your home after 2020, you will have to remain the owner of the property for at least 5 years.

If apartments are exchanged without additional payment, then you do not have to pay tax.

If there are several owners, the amount of tax and the need to pay it will be distributed for each separately.

Exchange with surcharge

If an apartment is exchanged with an additional payment (one of the participants in the transaction receives an additional amount of money, in addition to the new property), then the amount received is included in the tax mass - a fee must also be paid from it.

The exchange agreement specifies which property was received and what amount.

To calculate the tax, the cost of the apartment is taken (market value, unless otherwise specified in the contract), and an additional payment is added. The parties transfer the additional payment in the standard manner as when purchasing an apartment.

Tax must be paid by July 15 of the year in which the declaration is submitted.

The declaration is submitted to the Tax Inspectorate at the place of registration of the taxpayer. You must submit it before 30.04 of the year following the year in which the transaction was carried out. If the apartment has been owned for less than 3 years, then it is mandatory to submit a declaration indicating the object received under the exchange agreement, even if there was no additional payment.

How much will I have to pay when registering a transaction?

The amount of tax required to be paid in a real estate exchange transaction is determined based on the specific features of the exchange agreement, or more precisely:

- If the subject or subjects of the transaction were owned by the owners for less than 3 years, the amount of tax is determined according to the standard formula for the entire cost of the apartment or apartments.

- In a situation where there is an additional payment, the size of the tax base is determined exclusively from this amount.

Accordingly, if the cases presented above are combined with each other, then the amount of the surcharge and the cost of the entire apartment are summed up and, based on the resulting value, the tax required to be paid is calculated.

The tax calculation formula is also different for the situations presented above:

- For the first case, the tax amount is determined by the formula - (cost of the apartment - 1,000,000 rubles) * 0.13. For example, citizen Ivanov exchanges his apartment, which he has owned for 2 years and costs 4,000,000 rubles, for another. This means that he must pay a tax equal to - (4,000,000 - 1,000,000) * 0.13, or more precisely - 390,000 rubles.

- For the second case, that is, if there is an additional payment under the agreement, the person receiving the additional payment under the exchange agreement undertakes to pay tax, which is calculated using the formula - (amount of additional payment) * 0.13. For example, citizen Penochkin exchanges his apartment, the cost of which is 2,000,000 rubles, for an apartment worth 3,000,000 rubles, then the tax that he must pay to the state is equal to - (1,000,000 * 0.13), or more precisely - 130 000 rubles.

Tax base when registering a real estate exchange transaction

(Apartment cost Additional payment – 1,000,000) * 0.13

It is important to note that in situations where one apartment, the subject of a transaction, was with its owner (participant in the transaction) for less than 3 years, and the other apartment, also the subject of a transaction, was with its owner (another participant in the transaction) for more than 3 years , then only the owner of the apartment who has owned it for less than 3 years is obliged to pay the tax.

The calculation of the tax amount is carried out exclusively on the cost of his own apartment, that is, the price of the other subject of the transaction is not taken into account when calculating the tax base.

For general information, let us clarify that you can use a deduction or receive one based on the results of a transaction only if the following conditions are met:

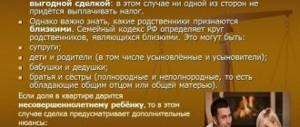

- The parties to the transaction are not interdependent persons. That is, if parents and their son are involved in an apartment exchange agreement, then obtaining or using a tax deduction is impossible. In the case of the participation of a family and their neighbor (not a relative) in the transaction, the tax deduction system is applicable.

- The party to the transaction who wishes to receive a deduction or take advantage of it pays personal income tax (personal income taxes). Everything is simple here, because such a measure is necessary only because it is from the personal income tax that the tax deduction is determined. Moreover, both in the situation with its receipt and with its use.

- The recipient of the deduction or the person using it has documentary evidence of the transaction. This measure is necessary in order to confirm the right to a tax deduction in authorized organizations. In the absence of such documents, the deduction is often not provided or is provided for a taxable base of 1,000,000 rubles, but no more.